Where should your next dollar go?

You’re earning more than ever – so why does every financial decision still feel overwhelming?

You’ve worked hard to get here. You have a good income, maybe a growing investment account, a 401(k) you’ve been contributing to, and a mental list of financial goals that keeps getting longer. You know you should be doing something smart with your money, but when you sit down to actually decide what, the options feel endless and the stakes feel high.

Should you max out your Roth IRA or contribute more to your traditional 401(k)? Pay off the mortgage early or invest the difference? Build up the emergency fund or put more into the market? Fund the kids’ 529 or focus on your own retirement first?

If any of that sounds familiar, you’re not alone and you’re not behind. You just don’t have a clear framework for prioritizing your next dollar.

Most people in their 30s, 40s, and 50s have absorbed plenty of financial advice over the years. The issue isn’t that they don’t know what a Roth IRA is. The issue is that they don’t know which of the ten smart things they could do right now is the right thing to do first.

Financial decisions don’t live in isolation. Putting money in the wrong place at the wrong time – even a technically “good” account – can cost you flexibility, trigger unnecessary taxes, or tie up capital you’ll need sooner than you expected.

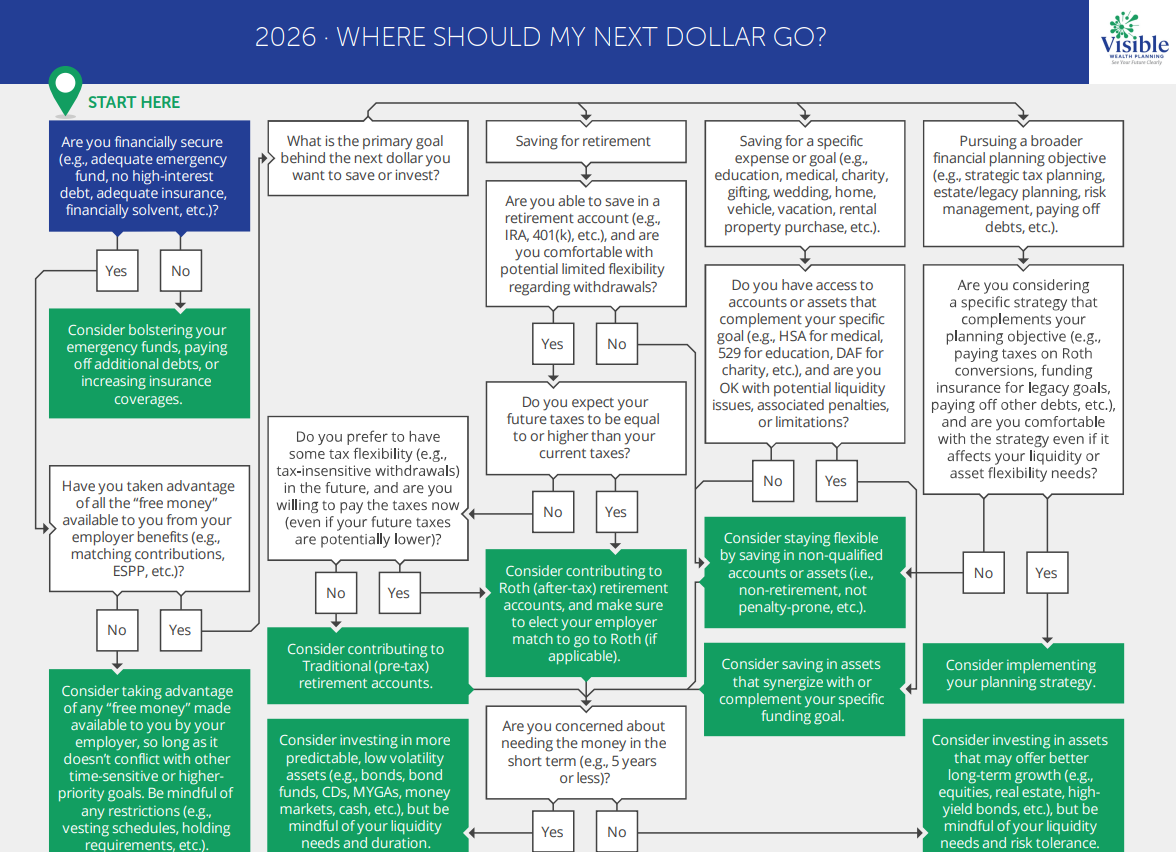

That’s why sequencing matters more than almost anything else in personal finance.

Start with these four questions

Before your next dollar goes anywhere, it helps to have clarity on a few things:

- Are you financially secure in the basics: emergency fund, insurance, no high-interest debt?

- What is this money actually for: retirement, a specific goal, long-term growth, or a broader strategy?

- How soon might you need access to it?

- What’s your current and expected future tax situation?

Your answers to those questions change everything about where that dollar should go. Someone who expects to be in a higher tax bracket in retirement should prioritize very differently than someone who expects to be in a lower one. Someone saving for a home purchase in three years needs a completely different approach than someone building a 20-year retirement portfolio.

We have a free, one-page flowchart called “Where should my next dollar go?” that walks you through exactly this decision, step by step, based on your actual situation. It will give you a clear starting point and help you ask the right questions before you act.

Download the guide and take the next step. If you’re ready to move from “I should probably do something” to an actual plan, we’re here to help, schedule your free 30-minute consultation. No pressure, no obligation – just clarity.