Demystifying Private Credit

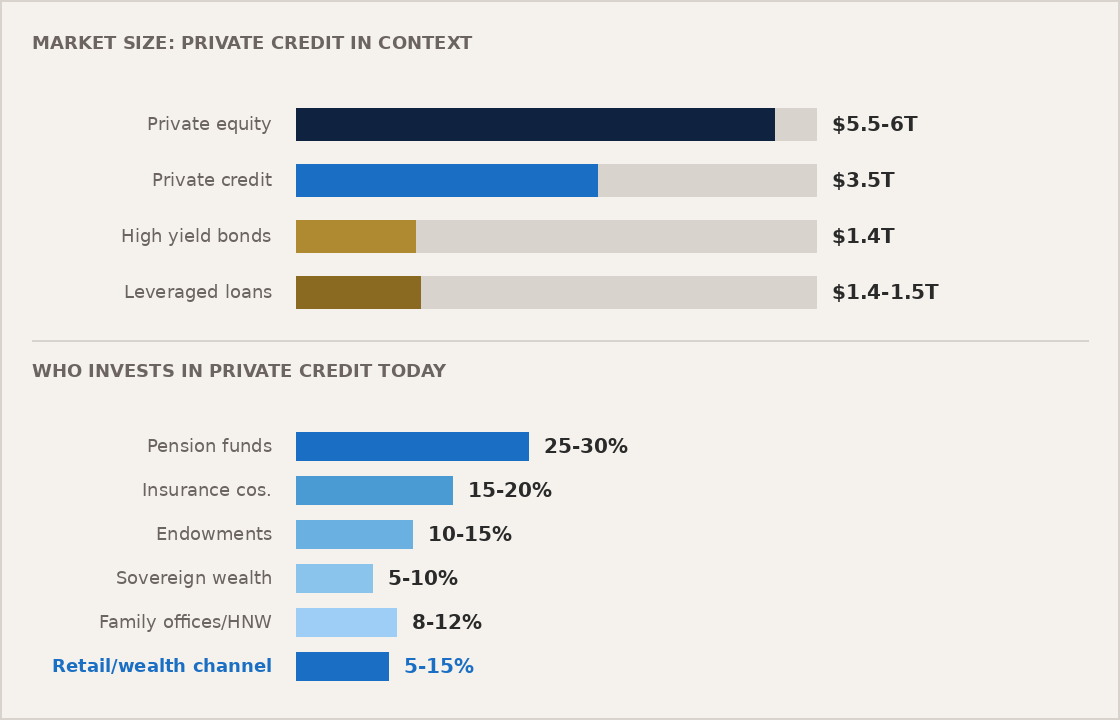

Private credit refers to loans made directly by investment funds rather than banks or public bond markets, typically to mid-sized companies needing flexible financing. It has grown into a $3.5 trillion market globally, roughly the size of the U.S. high yield bond and leveraged loan markets combined.

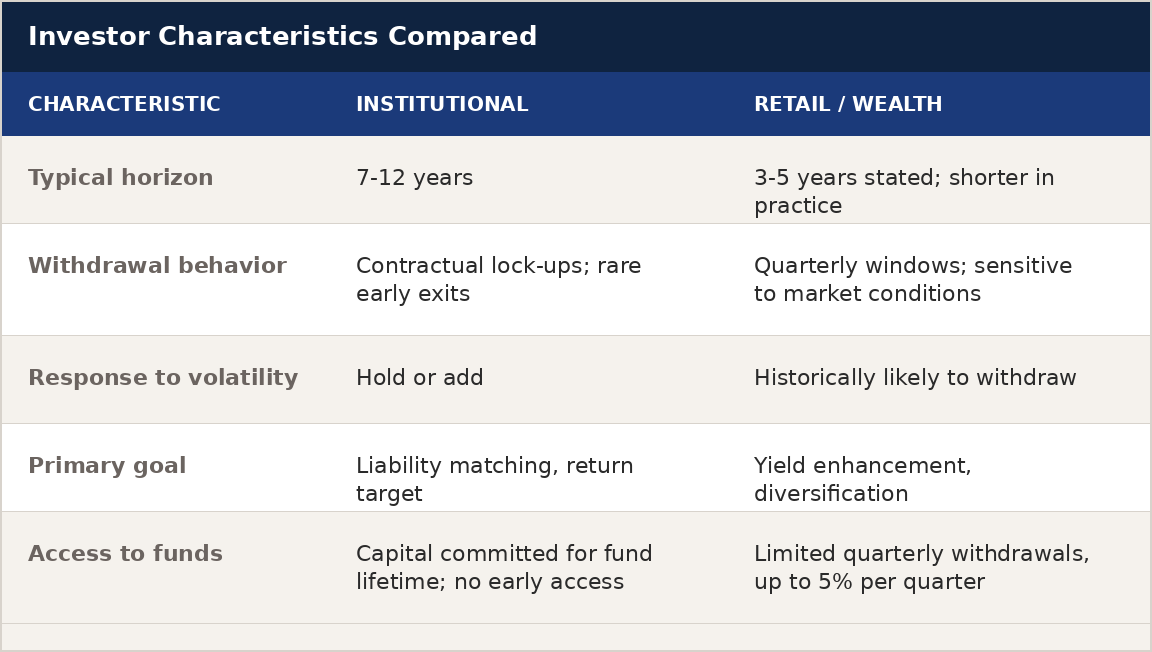

For most of its existence, private credit was the exclusive domain of large institutions: pension funds, insurance companies, endowments, and sovereign wealth funds. These investments offered strong returns and tended to behave differently from the stock market, helping with diversification. But the high minimum commitments, long lock-up periods, and regulatory complexity kept most individual investors out.

That changed in 2019, when new fund structures were created to broaden access. Two types of vehicles made this possible. An interval fund is a fund that allows investors to withdraw a limited amount of their money at set intervals, typically once per quarter, rather than being locked in for years. A BDC, or business development company, is a type of fund that lends directly to private companies and is available to individual investors. Both structures opened the door for financial advisors and their clients to invest in an asset class that had previously been out of reach.

Private credit expanded from roughly $1 trillion to approximately $3.5 trillion globally over the past five years. Increased access for individual investors has contributed to this growth, with capital flowing in through financial advisors and wealth platforms. Today, the wealth channel represents an estimated 5 to 15 percent of the market ($175 to $525 billion). That said, institutional investors remain the primary driver, and demand from companies seeking flexible financing outside of traditional banks has also played a significant role.

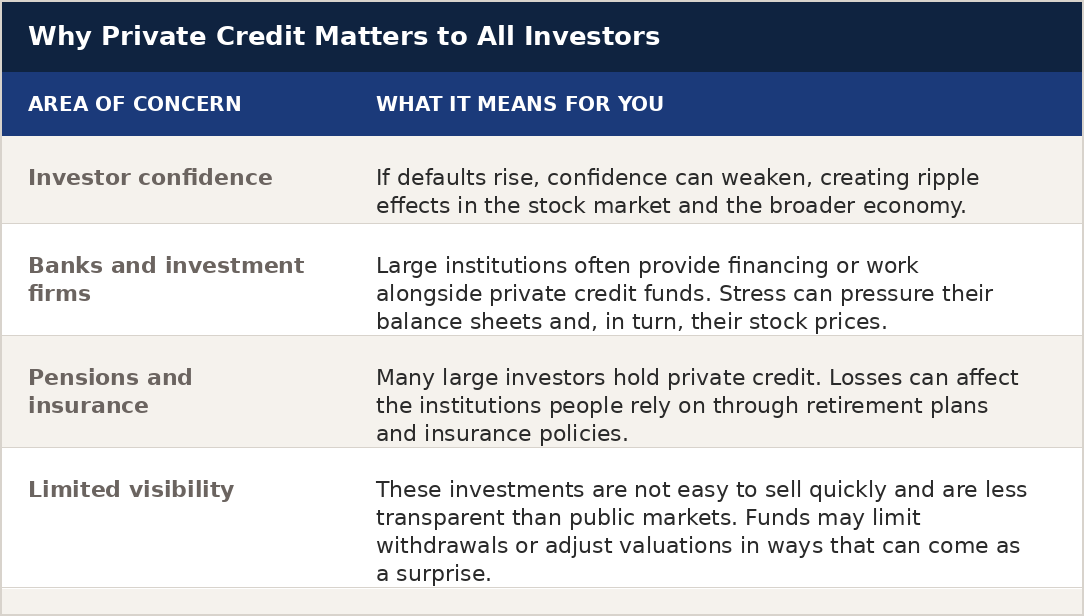

Stress in the private credit market matters even if you do not invest in it directly. As the market has grown, its connections to the broader financial system have deepened.

While private credit may seem like a niche area, its size and connections mean that problems can spread more broadly across the financial system.

In September 2025, two notable bankruptcies drew attention across credit markets. First Brands, an auto parts manufacturer, and Tricolor, a subprime auto lender, both failed after taking on significant debt. These events were notable not just because of the losses involved, but because they exposed real challenges in private credit: limited transparency, complex deal structures, and heavy reliance on lenders doing their own due diligence carefully.

A growing concern about artificial intelligence has added a separate layer of anxiety. Investors are questioning how AI may reshape entire industries and, more specifically, whether the technology and software companies that borrowed heavily in private credit markets over the past five years will remain competitive enough to repay those loans. This has prompted many investors to look more carefully at what their private credit funds actually own and whether the expected returns are still realistic.

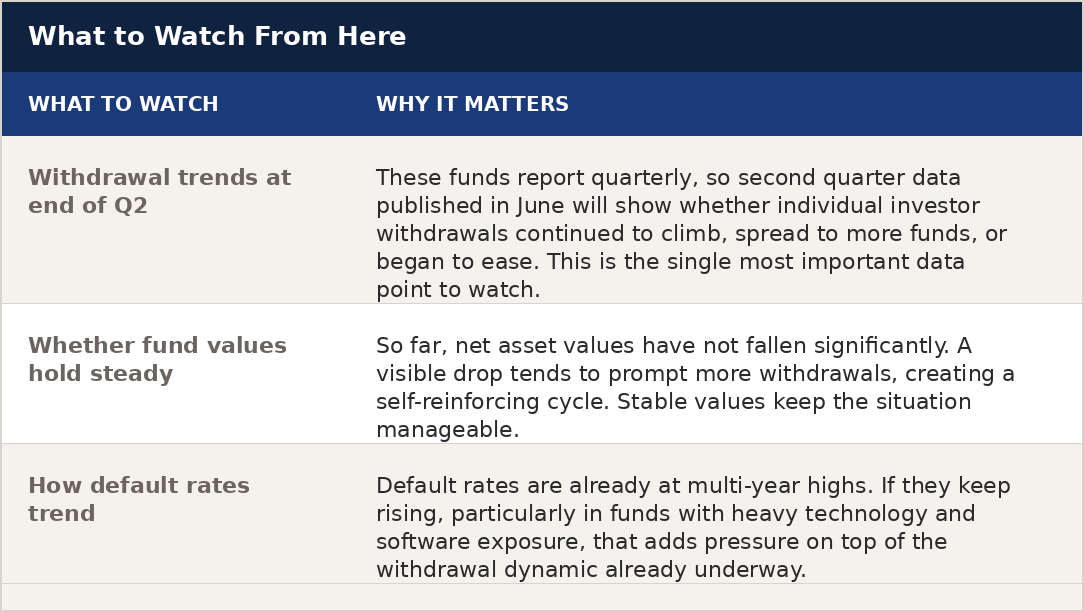

The anxiety building from both of these issues became very real in early 2026, when individual investors began pulling money out of private credit funds at a pace that caught many managers off guard. Most of these funds are designed to allow limited quarterly withdrawals, typically capped at 5 percent of assets. Several funds received requests well above that level. Managers responded differently: some honored withdrawals beyond the stated limit, others injected their own capital to meet requests without restricting access, and in a few cases funds enforced the cap or stopped withdrawals altogether.

The withdrawal pressure described above raises a deeper question, and it is not really about whether investors are sophisticated enough. It is about whether the structure of these funds matches how individual investors actually behave, especially when times get uncertain.

Large institutions like pension funds commit capital for many years at a time. Individual investors, even experienced ones, tend to want access to their money when markets get uncomfortable. The interval fund structure tries to bridge this gap by capping withdrawals at 5 percent per quarter. That limit is designed to prevent a fund from being forced to sell illiquid loans quickly at bad prices in order to return cash to departing investors.

| The real question is whether a strategy built for patient, long-term institutional capital can work well for individual investors who may need or want their money back sooner. |

According to reporting in the Financial Times, the elevated withdrawal requests we are seeing right now are concentrated in non-traded BDCs and interval funds. Institutional investors are largely not driving this trend. It is individual investors who are requesting their money back, which is precisely the dynamic these structures were supposed to guard against.

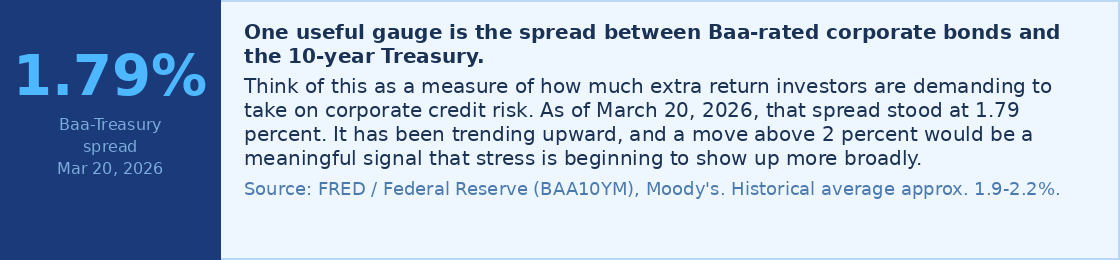

Overall, credit conditions today appear stable, but there are early signs worth paying attention to. For well-diversified funds holding thousands of loans across many industries, the outlook still looks relatively solid. That said, it is harder to make broad statements about the entire private credit market.

There are a few areas of specific concern. Default rates in private credit have been increasing and are now at their highest levels in several years. In addition, some funds have significant exposure to technology and software companies that were valued very highly in recent years. With rapid advances in artificial intelligence, there is growing uncertainty about how durable some of those business models will be.

Transparency is another consideration. Some funds invest through other funds or move loans between related entities, which can make it more difficult to see the underlying risks clearly. This does not mean there is a problem, but it does mean investors should be thoughtful and selective.

In short: credit quality is generally holding up, but there are enough emerging risks that this is an area to monitor closely.

The situation is still unfolding. Rather than predict how it plays out, here are the three things most worth paying attention to over the coming months.